Portfolio Planning

Lean Budgeting

A high level introduction to Lean Budgeting, capacity-led funding and implications for investment governance.

If you're new to Lean Portfolio Management and have not yet familiarised yourself with the concept of Value Streams - we strongly recommend that you start there. You can follow this link to take you straight to our introduction to value stream centric delivery.

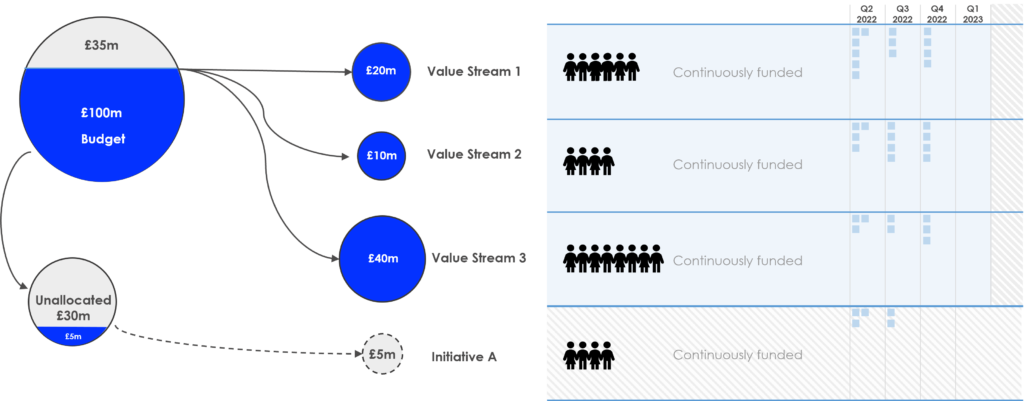

The key difference between traditional funding and Lean Budgeting is the concept of continuous funding. Rather than funding the project, you fund the value stream. Specifically, funding should cover the available capacity (i.e. permanent resources) that belong to each value stream.

The diagram below illustrates how to start thinking about this:

We will explore how we manage and allocate the “Unallocated” pot later.

When we then start to think about investment prioritisation, we must replace the concept of “how much will it cost” with “how much effort will it take my teams to achieve?"

But that doesn’t mean we totally lose sight of cost. Cost in Lean Budgeting becomes representative, rather than actual.

Let’s look at a simple example:

Cost in Lean Budgeting becomes representative, rather than actual.

Worked Example

Value Stream 1 costs $2million / year to operate. That’s predominately paying salaries, but other operating costs for the value stream too.

$2M

The total capacity of Value Stream 1, each quarter is 2000 days.

Over the course of a year, that’s 8000 days (4 x 2000).

Therefore the implied operating cost of that 8000 days of capacity is £2million.

8000 days

Let’s say we have assigned a piece of work to be delivered by Value Stream 1.

Value Stream 1 have estimated the piece of work to be 500 days of effort. That means that delivering this piece of work will consume 6.25% of Value Stream 1’s total capacity.

8000 days

500

days

The representative cost of this outcome is therefore $125,000 ($2M * 0.0625).

Note that this is the representative cost. It is useful to compare the value it is delivering, to the cost that it incurs. But if you choose not to deliver this outcome, you will still incur this cost. Either because the Value Stream will work on something else, or because they will be “idle”.

£2M

$125K

In the original diagram, you will have noticed that we have an allocated pot. This pot is reserved to fund additional capacity – for instance engaging third parties to accelerate or augment delivery. Or buying physical infrastructure for a specific initiative.

This unallocated funding can also be used to fund specific projects that do not fit within a value stream. These might be significant pan-organisation regulatory projects for example.

This mechanism is also helpful for organisations as they are transitioning from traditional portfolio management towards lean portfolio management. It allows organisations to configure “Temporary Value Streams” to support their traditional delivery as they iteratively and incrementally roll out Lean Portfolio Management across the organisation.

It means that the transition does not need to be seen as an “On/Off Switch” but rather an iterative journey towards agility.

Got questions? Confused? Get in touch and one of our experts can help you apply these concepts to your organisation.